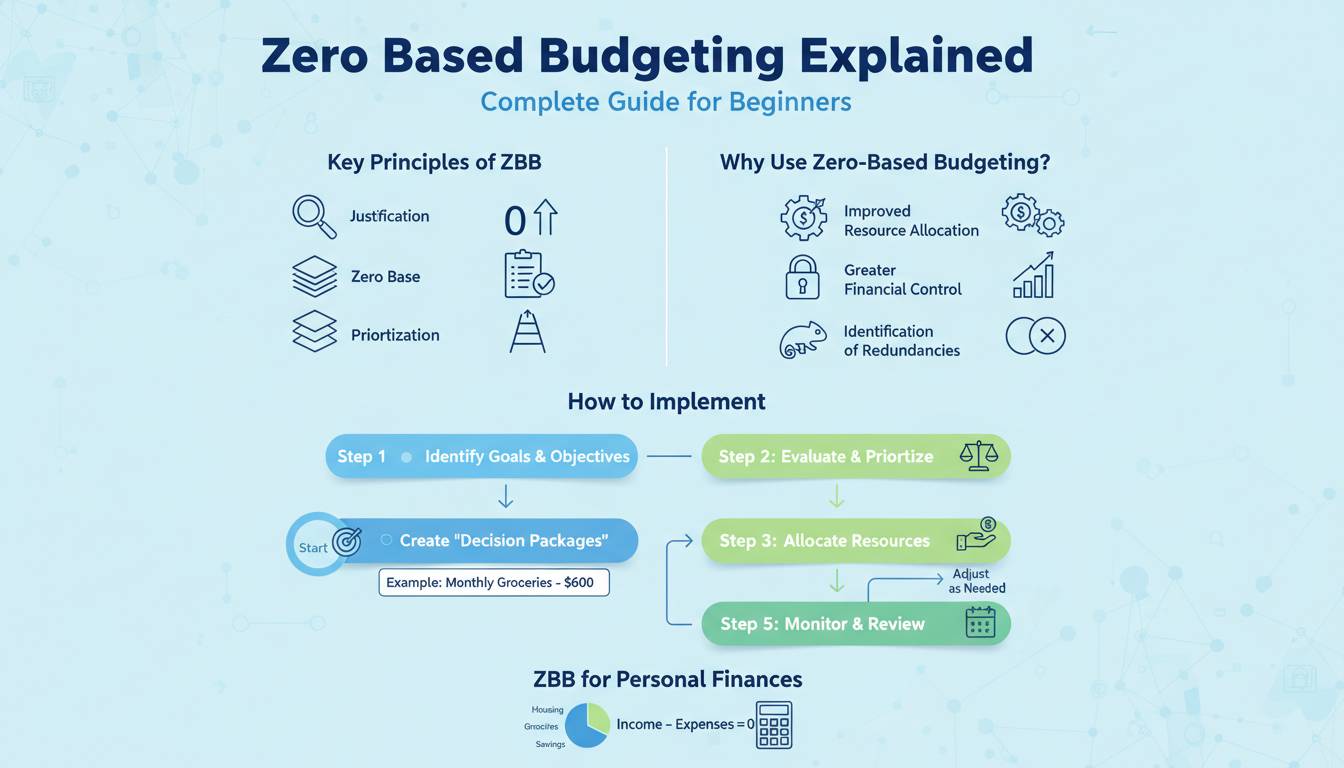

Zero based budgeting (ZBB) is a financial planning method where every dollar of income gets assigned a specific job before the month begins. Unlike traditional budgeting where you track spending after it happens, zero based budgeting requires you to give every single dollar an assignment—whether that’s bills, savings, debt payments, or discretionary spending. The goal is simple: reach “zero” by subtracting your income from your expenses and savings, leaving nothing unaccounted for.

This approach gained mainstream attention through Dave Ramsey’s popularization in the 1990s, though the methodology itself originated in the 1970s as a corporate budgeting technique. For individuals and families, zero based budgeting transforms how you think about money by eliminating the “what happened to my money?” confusion that plagues traditional budgeting methods.

What Is Zero Based Budgeting and How Does It Work?

Zero based budgeting works on a fundamental principle: your income minus your expenses plus savings must equal zero. This doesn’t mean you spend all your money—it means you plan for every dollar so that your available balance reaches zero by month’s end. If you earn $4,000 monthly and have $3,400 in planned expenses and $600 in savings contributions, you’re at zero. Nothing is left randomly sitting in your checking account.

The process begins with listing all income sources for the month, then systematically assigning dollars to each expense category. Common categories include housing (mortgage or rent), utilities, transportation, groceries, insurance, minimum debt payments, savings goals, and discretionary spending like entertainment and dining out. Each category receives a specific dollar amount based on your financial priorities and goals.

The critical difference from conventional budgeting: Most people add up their fixed expenses, subtract from income, and simply “see what’s left” for other categories. This approach almost always results in overspending because there’s no explicit plan for those remaining dollars. Zero based budgeting forces intentional decisions about every dollar before spending occurs.

Step-by-Step Process for Creating Your First Zero Based Budget

Step 1: Calculate Your Total Monthly Income

Gather all reliable income sources for the month. Include your primary salary, any side hustle earnings, alimony, child support, or regular gifts. Use your net income (after taxes) for accuracy, though some prefer budgeting from gross income and accounting for taxes separately. If your income fluctuates, use your lowest recent month or the average of the last three months.

Step 2: List All Expense Categories

Create categories covering every possible expense. Fixed expenses are easy—they remain constant monthly: rent or mortgage, car payment, insurance premiums, subscription services. Variable expenses require estimation: groceries, gas, utilities, entertainment. Don’t forget less frequent expenses like car maintenance, medical visits, or gifts—divide annual costs by 12 to find monthly averages.

Step 3: Assign Dollars to Each Category

Starting with fixed expenses, work through each category assigning specific amounts. Move to variable expenses, then savings and debt payments. If you run out of money before assigning all categories, you must reduce some allocations. If you have surplus money after all needs are met, assign it to debt payoff or savings. The key: you cannot have unassigned dollars.

Step 4: Track Throughout the Month

Your budget is merely a plan until you track actual spending. Record transactions daily using your preferred method—spreadsheet, app, or notebook. Compare actual spending to planned amounts weekly. When a category runs low, you must either reduce spending in that category or take money from another category where you underspent. This flexibility is what makes zero based budgeting work.

Step 5: Repeat and Refine Monthly

Budgeting improves with practice. Review the previous month’s results. Identify categories where you consistently underestimate or overestimate. Adjust future months based on actual behavior. Most people need three to four months before their budget feels comfortable and accurate.

Essential Categories for a Zero Based Budget

Creating effective categories requires balancing detail with simplicity. Too few categories hide spending patterns; too many become overwhelming to manage.

Fixed Monthly Expenses:

– Housing (rent/mortgage)

– Property taxes (if not escrowed)

– Homeowners or renters insurance

– Vehicle payment

– Vehicle insurance

– Health insurance premiums

– Life insurance

– Phone bill

– Internet/cable streaming services

– Student loan minimum payments

– Other loan minimums

Variable Expenses:

– Groceries

– Gas/transportation

– Utilities (electric, gas, water)

– Dining out/takeout

– Entertainment

– Personal care (haircuts, toiletries)

– Clothing

– Subscriptions not on fixed list

– Miscellaneous

Financial Goals:

– Emergency fund contributions

– Retirement account contributions

– Extra debt payments

– Savings for large purchases

– Investment contributions

– Vacation fund

Common Mistakes When Starting Zero Based Budgeting

Beginning budgeters consistently make predictable errors that undermine their success. Understanding these pitfalls helps you avoid them.

Mistake #1: Being Too Restrictive

New budgeters often set unrealistic category limits based on desired spending rather than actual behavior. When you allocate $200 for groceries but typically spend $350, you’ll fail every month. Start with reality, then gradually reduce categories by 5-10% as you identify waste.

Mistake #2: Forgetting Irregular Expenses

Annual or quarterly expenses blindside beginners. Car registration, appliance replacement, holiday gifts, annual subscriptions—these create budget disasters when they arrive unexpectedly. Track these expenses for one year, divide by 12, and create savings categories for each.

Mistake #3: Not Budgeting for Fun Money

Completely eliminating discretionary spending leads to budget burnout. Allocate a small “fun money” category with no guilt required. Whether it’s $50 monthly for coffee shops or $100 for entertainment, this buffer prevents complete budget abandonment after one bad week.

Mistake #4: Treating All Months Identically

Income fluctuates for many households. January differs from December. Summer may bring unexpected expenses. Adjust categories monthly based on known upcoming events, holidays, and income changes.

Best Zero Based Budgeting Apps and Tools

Several digital tools simplify zero based budgeting implementation. The best option depends on your technical comfort level and specific needs.

| App | Best For | Price | Key Features |

|---|---|---|---|

| YNAB (You Need A Budget) | Complete methodology adherence | $14.99/month or $109/year | Teaches zero based principles, goal tracking, debt payoff planning |

| EveryDollar | Ramsey method followers | Free version available; Plus $17.99/month | Simple interface, budget templates, bank linking |

| Monarch Money | Comprehensive financial view | $15/month | Aggregates all accounts, automatic categorization, net worth tracking |

| Goodbudget | Envelope method users | Free version; Plus $10/month | Envelope system, good for couples, debt tracking |

| Spreadsheet | DIY flexibility | Free | Complete control, customizable, requires more manual work |

YNAB stands out for teaching the methodology while providing robust tools. Its four rules—give every dollar a job, embrace your true expenses, roll with the flexibility, and age your money—directly align with zero based budgeting principles. The learning curve is worth the effort for serious budgeters.

EveryDollar appeals to followers of Dave Ramsey’s approach. The free version works well; the paid version adds bank synchronization. Its simplicity makes it ideal for absolute beginners uncomfortable with complex financial tools.

How Zero Based Budgeting Differs from Other Budgeting Methods

Understanding how zero based budgeting compares to alternatives helps you choose the right system or combine approaches.

Zero Based vs. Pay Yourself First

Pay yourself first prioritizes savings before expenses, automatically directing money to retirement and emergency funds. It doesn’t address how remaining income gets spent. Zero based budgeting incorporates this principle but adds detailed planning for all categories.

Zero Based vs. 50/30/20 Rule

The 50/30/20 rule allocates percentages: 50% to needs, 30% to wants, 20% to savings. It’s simpler but less precise. Zero based budgeting creates granular control while requiring more effort.

Zero Based vs. Envelope Budgeting

Envelope budgeting uses physical or digital “envelopes” for spending categories. When an envelope empties, spending stops. Zero based budgeting serves the same purpose through digital tracking rather than cash management.

Zero Based vs. Anti-Budget

Some financial writers advocate for “anti-budget” approaches—simply saving automatically and spending freely on non-essential items without tracking. This works for high-income individuals with strong self-control. Zero based budgeting suits those who need structure and accountability.

Real Results: Who Benefits Most from Zero Based Budgeting

Zero based budgeting delivers the greatest impact for specific financial situations.

Debt Payoff Enthusiasts

When you’re aggressively paying off credit cards or student loans, zero based budgeting identifies every available dollar for debt payments. The visibility into all spending categories reveals hidden money for accelerated payoff. One couple using this method paid off $47,000 in credit card debt in 18 months by finding $600 monthly in unused budget categories.

Income Fluctuation Workers

Freelancers, commission-based salespeople, and seasonal workers benefit enormously. Assigning dollars to categories before knowing your exact income forces prioritization and prevents overspending during high-earning months. Many contractors build three-month rolling budgets rather than monthly.

Couples and Families

Shared finances require communication. Zero based budgeting creates structured discussions about money priorities. When both partners see exactly where every dollar goes, negotiations become objective rather than emotional. Weekly budget meetings become planning sessions rather than arguments.

Savers with No Plan

High earners who save significantly but lack specific goals benefit from intentional assignment. A person earning $120,000 annually who saves $2,000 monthly “because they should” might redirect those dollars toward a house down payment, retirement acceleration, or business investment when forced to make explicit decisions.

Getting Started: Your First Zero Based Budget in 60 Minutes

You can create your initial zero based budget in under an hour using this streamlined process.

Preparation (15 minutes):

Gather last three months of bank and credit card statements. Calculate average monthly income. Create a simple spreadsheet or open your chosen app.

Categorization (20 minutes):

List every expense from your statements. Group similar items into categories. Add categories for expenses you know exist but don’t appear on statements (cash spending, irregular items).

Assignment (15 minutes):

Enter your income at the top. Starting with fixed expenses, assign dollar amounts to each category. Work through all categories until you reach zero.

Validation (10 minutes):

Review for reasonableness. Can you actually live on $350 groceries? Did you forget entertainment? Adjust until the budget feels challenging but achievable.

Commit (moment):

Start tracking immediately. Your first month will be imperfect—that’s normal. The discipline comes from doing it again month after month, refining each iteration.

Frequently Asked Questions

How long does it take to create a zero based budget?

Your first budget takes approximately 45-60 minutes. After establishing categories, subsequent months require 15-20 minutes for adjustments based on income changes or spending pattern insights. Most users report that monthly maintenance becomes a 10-minute task after the initial learning period.

Do I need to use cash for zero based budgeting?

No. While envelope budgeting uses cash, zero based budgeting works with any payment method. Digital tracking offers advantages: automatic categorization, transaction history, and reduced time investment. The methodology focuses on planning and assignment rather than payment medium.

What if my income varies month to month?

Use your lowest monthly income from the past year as your baseline. Budget that amount strictly. When higher income arrives, the surplus automatically becomes extra debt payments or savings. Alternatively, maintain a buffer in your checking account equal to one month’s expenses to smooth income fluctuations.

Can I still use credit cards with zero based budgeting?

Yes, credit cards work perfectly within zero based budgeting. Simply record credit card purchases against their relevant categories when they occur. The key: track spending in real-time rather than waiting for statements. Many budgeters pay credit cards weekly to avoid losing track of accumulated debt.

What if I go over budget in one category?

Zero based budgeting anticipates category overruns. The “rule” is that you must reduce another category to cover the overspend. This maintains your zero balance commitment. In practice, you “roll with the punches”—borrow from categories where you underspent and accept that no category is untouchable.

How long before zero based budgeting becomes habitual?

Most people need 60-90 days before budgeting feels automatic. The first month involves constant attention. The second month becomes easier as categories stabilize. By the third month, you think about spending differently—asking “is this in my budget?” before purchases becomes automatic.

Conclusion: Is Zero Based Budgeting Right for You?

Zero based budgeting isn’t the only effective financial system, but it offers unique advantages for those willing to invest the initial effort. The methodology provides complete visibility into your financial life, forces intentional decisions about money, and creates accountability that prevents the unconscious overspending plaguing most households.

If you struggle with “where did all my money go?” moments at month’s end, feel uncomfortable with your spending patterns, or want to accelerate debt payoff or savings, zero based budgeting delivers results. The 30-45 minutes weekly required for maintenance is minimal compared to the financial clarity gained.

Start this month. Download an app, grab your bank statements, and assign every dollar a job. The first budget won’t be perfect—but it will be the beginning of a transformed relationship with your money.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment