Credit card interest rates, expressed as Annual Percentage Rates (APR), directly impact how much debt costs over time. With average rates hovering above 20% and balances growing across American households, understanding these numbers isn’t optional—it’s essential for financial survival.

📊 KEY STATS

– The Federal Reserve reports the average credit card APR is 24.37% as of late 2024, a record high

– Americans carry $1.14 trillion in credit card debt (Federal Reserve Bank of New York)

– Households with credit card debt pay an average of $1,300+ annually in interest alone

– 67% of cardholders don’t know their current APR (CreditCards.com survey)

Understanding how interest compounds, when it’s applied, and how to avoid it puts thousands of dollars back in your pocket annually. This guide breaks down everything you need to know about credit card interest rates, from the mechanics of APR calculation to proven strategies for minimizing what you pay.

What Is Credit Card APR?

Annual Percentage Rate (APR) represents the yearly cost of borrowing money on your credit card, including interest and fees, expressed as a percentage. Unlike simple interest, APR accounts for how often interest compounds—the more frequent the compounding, the higher your effective rate.

Credit card APRs typically range from about 15% to 30%, with the exact rate determined by your creditworthiness, the card type, and market conditions. Prime borrowers with excellent credit might secure rates around 17-19%, while those with fair or poor credit may face rates of 25% or higher.

Why APR Matters More Than the Interest Rate

When credit card companies advertise rates, they often show the “periodic rate”—the interest charged per billing cycle. However, this number can be misleading because it doesn’t reflect how interest compounds. The APR standardizes this, giving you a true picture of annual borrowing costs.

For example, a card with a 1.5% monthly periodic rate (18% APR) actually costs more than you might realize because interest charged in month one accrues interest in month two—a process called compounding. Over a full year, the effective rate can exceed the stated APR slightly, though federal regulations now require card issuers to disclose this clearly.

The Role of the Prime Rate

Most credit card APRs are variable, meaning they fluctuate based on the prime rate—the interest rate banks charge their most creditworthy corporate borrowers. The Federal Reserve sets the federal funds rate, which influences the prime rate indirectly. When the Fed adjusts its rate, credit card APRs typically move in the same direction within one to two billing cycles.

As of 2024, the prime rate sits at approximately 8.5%, meaning credit card issuers add a margin of 10-17 percentage points above prime to determine individual cardholder rates. This relationship explains why your APR changed after Federal Reserve rate adjustments over the past two years.

Types of Credit Card APR

Credit cards don’t have a single APR. Understanding the different types helps you recognize when each applies and potentially avoid costly charges.

| APR Type | Typical Range | When It Applies |

|---|---|---|

| Purchase APR | 15% – 29% | Regular card purchases |

| Balance Transfer APR | 0% – 29% | Transferred balances from other cards |

| Cash Advance APR | 25% – 30% | ATM withdrawals, cash equivalents |

| Penalty APR | Up to 35% | Late payments, default triggers |

| Introductory APR | 0% | Promotional period (typically 12-21 months) |

Purchase APR

This is the standard interest rate applied to new purchases when you carry a balance from month to month. If you pay your full statement balance by the due date, you won’t pay any purchase interest—this is the grace period credit card issuers provide.

Balance Transfer APR

Many cards offer 0% balance transfer APR promotions, allowing you to move high-interest debt from other cards and pay it down interest-free for a set period. These promotions typically last 12-21 months. However, most cards charge a balance transfer fee of 3-5% of the transferred amount, which can offset savings if you’re not careful.

After the promotional period ends, any remaining balance converts to the card’s regular APR—often higher than what you were paying originally.

Cash Advance APR

Cash advances—including ATM withdrawals, wire transfers, and traveler’s checks—typically trigger the highest APR, sometimes exceeding 30%. Additionally, most cards don’t offer a grace period for cash advances; interest starts accruing immediately from the transaction date.

Penalty APR

Miss a payment by 60 days or more, or exceed your credit limit, and issuers may impose a penalty APR—sometimes as high as 35.99%. This rate applies to new purchases and can even apply retroactively to existing balances. The good news: under the CARD Act of 2009, penalty APRs must revert to the original rate after six months of on-time payments.

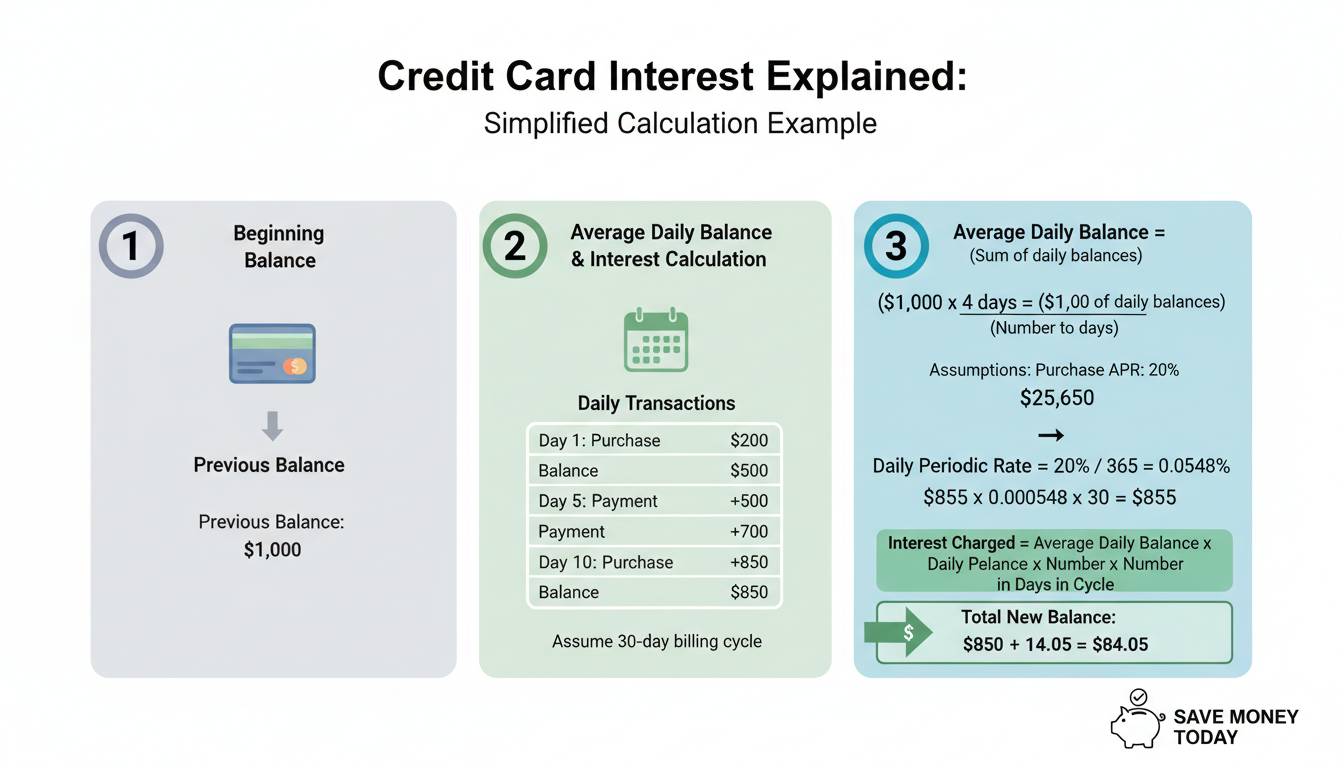

How Credit Card Interest Is Calculated

Understanding the calculation mechanics reveals why carrying even small balances costs more than you might expect.

The Daily Balance Method

Most U.S. credit card issuers use the daily balance method to calculate interest:

Step 1: Convert your APR to a daily periodic rate by dividing by 365 (some issuers use 360)

Step 2: Calculate your average daily balance by adding each day’s balance and dividing by the billing cycle days

Step 3: Multiply the daily periodic rate by the average daily balance, then multiply by the number of days in the billing cycle

Example: If your APR is 24% and your average daily balance is $2,000 across a 30-day billing cycle:

– Daily rate: 24% ÷ 365 = 0.06575%

– Daily interest: $2,000 × 0.0006575 = $1.315

– Monthly interest: $1.315 × 30 = $39.45

The Importance of the Grace Period

The grace period is the time between your statement closing date and payment due date—typically 21-25 days. If you pay your full statement balance by the due date, you avoid interest entirely on purchases.

However, this protection vanishes the moment you carry a balance. If you pay $1,900 of a $2,000 balance, the remaining $100 starts accruing interest immediately, and new purchases also accrue interest because you’re no longer in a grace period.

Compounding: The Silent Cost Multiplier

Interest doesn’t just accumulate on your principal balance—it compounds. When interest is added to your balance, that interest itself earns interest in subsequent periods. This exponential growth is why carrying debt becomes increasingly expensive over time.

Current Market Rates and Trends

Credit card interest rates have reached historic highs, reflecting both Federal Reserve policy changes and issuer risk assessments.

📊 MARKET OVERVIEW

| Metric | Current Rate | Year-Ago Rate |

|——–|————–|—————|

| Average APR (all cards) | 24.37% | 22.16% |

| Average APR (new offers) | 24.75% | 23.43% |

| Lowest available APR | 0% (promo) | 0% (promo) |

| Highest standard APR | 36% | 36% |

The Federal Reserve’s 11 rate increases between 2022 and 2023 directly impacted variable-rate credit cards, pushing average rates up by approximately 5 percentage points. While the Fed has held rates steady in 2024, credit card APRs remain near all-time highs.

Regional and Demographic Variations

Credit card rates vary significantly based on credit score tiers:

| Credit Score | Average APR Offered |

|---|---|

| 720-850 (Excellent) | 16.65% |

| 690-719 (Good) | 19.87% |

| 630-689 (Fair) | 24.91% |

| Below 630 (Poor) | 28.15% – 32% |

Geographic factors also play a role. Residents of states with higher average debt burdens or cost-of-living expenses sometimes face slightly higher rates from certain issuers, though this varies by lender.

Strategies to Avoid Paying Interest

Paying zero interest on credit cards is entirely possible with the right habits and strategies.

Always Pay the Full Statement Balance

The most straightforward method: pay your complete statement balance by the due date every month. This maintains your grace period and avoids interest entirely on purchases. This approach requires discipline but costs nothing and builds credit history.

Use Balance Transfer Cards Strategically

For existing debt, 0% balance transfer cards can provide 12-21 months of interest-free repayment. Key strategies:

- Calculate the break-even point: Compare the balance transfer fee (typically 3-5%) against the interest you’d pay on your current card. If the promo saves more than the fee, the transfer makes sense.

- Create a payoff plan: Treat the promotional period as a deadline. Divide your balance by the number of months to determine your required monthly payment.

- Avoid new purchases: Most cards apply payments to the lowest-interest balance first, meaning new purchases at regular APR can linger unpaid.

Request a Rate Reduction

Credit card issuers have more flexibility on rates than many consumers realize. Calling and politely requesting a lower APR—citing your payment history, tenure as a customer, and competing offers—successfully reduces rates approximately 40% of the time according to industry surveys.

Consider a Personal Loan Consolidation

For large balances, a personal loan with a lower fixed interest rate (typically 8-15% for those with good credit) can consolidate credit card debt at a significantly reduced cost. The structured repayment term also forces faster payoff.

Common Mistakes Costing You Money

Many cardholders unknowingly pay more interest than necessary through preventable errors.

Mistake #1: Paying the Minimum

Paying only the minimum due keeps your grace period inactive, meaning all new purchases immediately accrue interest. A $5,000 balance at 24% APR with minimum payments (typically 2% of balance or $25, whichever is higher) takes over 27 years to pay off and costs more than $12,000 in total interest.

Better approach: Pay as much as possible above the minimum, focusing on the highest-APR balances first.

Mistake #2: Missing Payment Due Dates

A single late payment can trigger penalty APRs of 30% or higher and damage your credit score significantly. Additionally, issuers typically apply any payments to the lowest-interest balance first, leaving high-interest debt untouched.

Protection strategy: Set up automatic minimum payments, then manually pay more when possible.

Mistake #3: Ignoring the Intro Rate Expiration

When promotional 0% APR periods end, the remaining balance converts to the regular APR—often much higher than expected. Calendar reminders 60 days before promo expiration give you time to pay down the balance or transfer it again.

Mistake #4: Using Cards for Cash Advances

Avoid cash advances whenever possible. The combination of higher APR (no grace period), transaction fees (typically 3-5%), and ATM fees makes this the most expensive way to access cash.

Frequently Asked Questions

What is a good credit card interest rate?

A good rate depends on your credit score, but for those with excellent credit (720+), rates around 15-18% are competitive. Good credit (690-719) typically qualifies for 18-22%. Any rate above 25% should prompt consideration of alternatives or a rate negotiation request.

How is credit card interest different from other loan interest?

Credit card interest is unique because it operates on a revolving basis with a grace period—if you pay in full monthly, you pay zero interest. Other loans (auto, mortgage) don’t offer this flexibility and typically have lower rates because they’re secured by collateral.

Can I negotiate my credit card interest rate?

Yes. Call your card issuer’s customer service line, ask to speak with a representative about rate reduction, and mention your payment history, tenure, and any competing offers you’ve received. Many customers successfully secure reductions of 5-10 percentage points.

Does carrying a small balance help my credit score?

No—this is a common myth. Carrying a balance does not improve your credit score compared to paying in full. Payment history (35% of your score) and credit utilization (30%) matter most. You can build credit history by using cards and paying the full balance monthly.

What happens when my 0% APR promotional period ends?

Any remaining balance converts to the card’s regular APR, typically 20-29%. Interest starts accruing immediately on that balance. To avoid surprises, set calendar reminders 60-90 days before promo expiration to either pay off the balance or initiate a new balance transfer.

How do I calculate how much interest I’ll pay?

Use this formula: (APR ÷ 365) × Average Daily Balance × Days in Billing Cycle. Most card issuers provide this calculation in your monthly statement. Online calculators from Bankrate, NerdWallet, or CreditCards.com can also estimate costs based on your specific balance and rate.

Conclusion

Credit card interest rates don’t have to drain your finances. Understanding how APR works—different types, calculation methods, and the impact of compounding—gives you the knowledge to make smarter borrowing decisions. The average 24% APR means every $1,000 carried costs roughly $240 annually in interest alone.

The most powerful strategy remains the simplest: pay your full statement balance monthly to maintain the grace period and avoid interest entirely. For existing debt, leverage balance transfer promotions, request rate reductions, or consider consolidation through a lower-interest personal loan.

Your credit card interest rate isn’t fixed in stone. With good payment habits, strategic use of promotional offers, and proactive communication with issuers, you can significantly reduce what you pay—or eliminate interest costs altogether. The money you save stays in your pocket, working toward your own financial goals rather than enriching card issuers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment