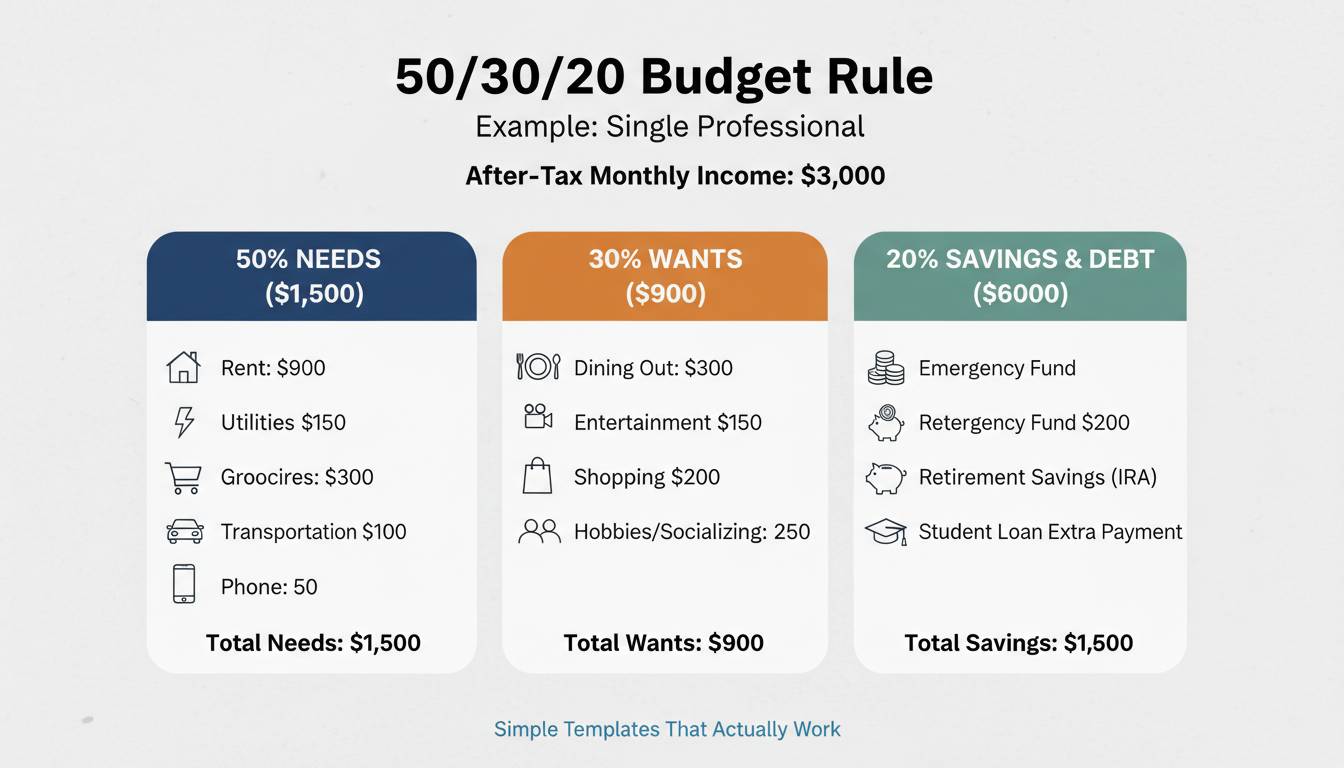

The 50/30/20 budget rule has become one of the most talked-about budgeting frameworks in personal finance—and for good reason. Developed from Senator Elizabeth Warren’s research at Harvard Law School, this simple formula provides a balanced approach to managing money without requiring obsessive tracking or complicated spreadsheets. Instead of telling you to cut every discretionary expense, it gives you permission to enjoy your money while still building financial security.

Whether you earn $30,000 or $150,000 per year, the 50/30/20 rule scales to fit your situation. The key is understanding what actually counts as a “need” versus a “want,” and how to apply these percentages to your specific after-tax income. This article provides concrete examples across different income levels and life situations, so you can see exactly how this budgeting method works in practice.

Understanding the 50/30/20 Rule Basics

Before diving into examples, let’s clarify what each category actually includes, because this is where most people get stuck.

The 50% needs category covers everything essential for survival and basic functioning: rent or mortgage payments, utilities, groceries, insurance premiums, minimum credit card payments, car payments for essential transportation, and healthcare costs. These are expenses you would have difficulty eliminating without serious consequences to your safety or health.

The 30% wants category encompasses everything that makes life enjoyable but isn’t strictly necessary: streaming subscriptions, dining out, entertainment, hobbies, gym memberships, travel, clothing beyond basic necessities, and gadgets. This category exists because financial wellness isn’t just about maximization—it’s about balance.

The 20% savings category includes everything that builds your financial future: emergency fund contributions, retirement account deposits, extra debt payments beyond minimums, investment contributions, and savings for major purchases. This is the foundation of long-term financial security.

Here’s the critical detail most articles skip: these percentages apply to your after-tax income, not your gross salary. If you earn $60,000 annually and take home $48,000 after taxes, your 50/30/20 calculations start from $48,000, not $60,000.

Example 1: The Entry-Level Professional

Meet Sarah, a 25-year-old marketing coordinator living in Columbus, Ohio. She earns $42,000 per year with approximately $2,800 in monthly take-home pay after taxes and deductions.

Using the 50/30/20 rule, Sarah’s budget breaks down as follows:

Needs ($1,400):

- Apartment rent: $950

- Utilities (electric, gas, water, internet): $150

- Groceries: $200

- Car payment and insurance: $180

- Minimum credit card payment: $50

- Phone plan: $70

Wants ($840):

- Streaming services (Netflix, Spotify): $30

- Dining out and takeout: $250

- Entertainment (movies, events): $100

- Shopping and hobbies: $200

- Gym membership: $60

- Travel savings: $200

Savings ($560):

- Emergency fund: $300

- Employer 401(k) match: $160 (she contributes 5% and gets 4% match)

- Extra debt payment: $100

Sarah was surprised to discover that her actual spending closely matched the rule’s recommendations once she categorized her expenses honestly. The biggest eye-opener was realizing that her $250 monthly dining out budget was more than double what she’d estimated. This awareness alone helped her make more intentional choices about when to eat out versus cook at home.

Example 2: The Dual-Income Family

Marcus and Keisha are a married couple in Houston with two children ages 8 and 12. Marcus earns $75,000 as an IT manager, and Keisha earns $65,000 as a registered nurse. Their combined after-tax monthly income is approximately $9,200.

Needs ($4,600):

- Mortgage (principal, interest, property taxes): $2,200

- Utilities: $350

- Groceries: $800

- Health insurance premiums: $450

- Car payments (two vehicles): $500

- Minimum debt payments: $150

- Childcare/before-after school care: $400

Wants ($2,760):

- Streaming and subscriptions: $80

- Dining out: $400

- Family entertainment: $300

- Kids’ extracurricular activities: $250

- Vacations/travel fund: $500

- Home maintenance fund: $300

- Miscellaneous wants: $430

- Shopping: $500

Savings ($1,840):

- Emergency fund: $500

- 401(k) contributions (they max employer match): $800

- 529 college savings plans: $400

- Extra mortgage payment: $140

This family faces the challenge many dual-income households encounter: their “needs” category runs slightly over 50% due to Houston’s competitive housing market and childcare costs. Rather than viewing this as failure, they made a conscious decision to prioritize wants slightly less and savings slightly more in other months. They also maintain a flexible “needs” review every six months to ensure their categories remain accurate as circumstances change.

Example 3: The High Earner in a High-Cost City

David is a 34-year-old software engineer in San Francisco earning $180,000 annually. After federal and state taxes, his monthly take-home is approximately $10,500.

Needs ($5,250):

- Rent (one-bedroom apartment in Mission District): $3,200

- Utilities and internet: $180

- Groceries: $400

- Car payment, insurance, gas: $350

- Health insurance: $280

- Phone and miscellaneous: $140

- Minimum debt payments: $0 (he has no debt)

- Student loan minimum: $200 (he pays extra)

Wants ($3,150):

- Dining out and bars: $800

- Entertainment and events: $400

- Travel: $600

- Hobbies (rock climbing, photography): $300

- Subscriptions: $100

- Shopping: $450

- Fitness (gym, classes): $200

- Professional development: $300

Savings ($2,100):

- 401(k) contribution (he maxes out employer match at $1,000): $1,000

- HSA contribution: $200

- Brokerage account: $600

- Emergency fund: $300

David’s example illustrates how high earners can struggle with the 50/30/20 rule despite substantial income. San Francisco’s housing costs push his needs category significantly over 50%. However, he’s comfortable with this trade-off because his career opportunities in the Bay Area significantly outweigh the housing costs. The lesson here: the rule provides guidance, but your specific circumstances may require flexibility.

Example 4: The Freelancer with Variable Income

Jessica is a freelance graphic designer in Denver with fluctuating monthly income. In a good month, she earns $6,000; in slower months, $3,500. She uses a 12-month average of $4,800 for budgeting purposes.

Using the 12-month average ($4,800):

Needs ($2,400):

- Rent: $1,500

- Utilities: $200

- Groceries: $350

- Health insurance ( marketplace plan): $300

- Car payment: $250

- Phone: $80

- Business expenses (software, internet): $150

- Minimum tax payments: $200 (she sets aside for quarterly taxes)

Wants ($1,440):

- Dining and entertainment: $400

- Subscriptions: $60

- Shopping: $250

- Travel: $300

- Hobbies: $180

- Personal care: $150

- Miscellaneous: $100

Savings ($960):

- Emergency fund (she’s building to 6 months): $500

- Retirement (SEP-IRA): $300

- Business savings: $160

Jessica’s approach demonstrates how variable-income workers adapt the 50/30/20 rule. She budgets based on her conservative 12-month average rather than her best months, which prevents overspending during slow periods. She also maintains a larger emergency fund (nine months of expenses) due to income volatility. When income exceeds her average, the extra goes directly to savings.

Common Categories Misclassified by Beginners

Understanding what belongs in each category requires honest self-reflection. These misclassifications consistently trip up budget beginners.

Many people mistakenly place their gym membership in “needs” when it’s actually a “want.” Unless a doctor has prescribed exercise for a specific medical condition, your gym membership falls into the wants category. The same applies to premium cable or streaming packages, coffee shop visits, and subscription boxes—these enhance your life but aren’t essential.

Conversely, some beginners undercategory essential expenses. Life insurance premiums, particularly term life insurance if you have dependents, absolutely belong in needs. So do required professional memberships for your career, minimum debt payments you can’t avoid, and basic clothing for work.

The question to ask yourself: “Could I survive without this for a month without significant hardship?” If the answer is yes, it’s likely a want. If losing it would cause genuine problems beyond inconvenience, it’s a need.

How to Adapt the Rule to Your Situation

The 50/30/20 rule works as a guideline, not a rigid law. Here’s how to adjust it for different circumstances.

If you’re paying off high-interest debt (credit cards, personal loans), consider temporarily shifting your wants category down to 25% and directing the extra 5% to debt payoff. This accelerates your debt-free timeline significantly. Once the debt is gone, you can redistribute those percentages.

If you live in an area with exceptionally high housing costs (think New York, San Francisco, Los Angeles), your needs category may legitimately exceed 50%. Rather than stressing, adjust your percentages to 60/20/20 or even 70/15/15 temporarily. Your goal is sustainable progress, not perfection.

If you’re early in your career with low income, the 50/30/20 rule might feel impossible. In this case, aim for smaller percentages in savings initially—even 10% is better than nothing. As your income grows, gradually increase your savings rate.

Retirees on fixed incomes often find the rule’s wants category too generous. Many successfully adapt to a 60/10/30 split, with increased savings (including in retirement accounts) and reduced wants spending.

Practical Steps to Implement This Budget

Starting a new budget requires system setup before tracking begins.

First, calculate your actual after-tax monthly income. Don’t estimate—pull your most recent pay stubs or bank statements to get an accurate number. If you’re self-employed, calculate your average monthly income from the past 12 months.

Second, categorize your existing expenses by reviewing three months of bank and credit card statements. Most online banking apps let you export this data to spreadsheet software. Group each transaction as needs, wants, or savings.

Third, compare your current percentages to the 50/30/20 targets. The gap between your current spending and the recommended percentages shows your adjustment opportunities.

Fourth, make incremental changes. If your wants spending is currently 40% of income, don’t try to drop to 30% overnight. Aim for 35% this month, 32% next month, and 30% within a few months.

Finally, review and adjust monthly. Your first budget won’t be perfect, and that’s fine. Regular review lets you course-correct and refine your categories.

Frequently Asked Questions

Can I use the 50/30/20 rule if I’m self-employed?

Yes, absolutely. Self-employed individuals should calculate their budget using their 12-month average income rather than any single month’s earnings. This provides stability when income fluctuates. You’ll also need to account for self-employment taxes and quarterly estimated tax payments within your budget. Many freelancers find success by treating their tax obligations as a “need” expense.

What if my needs exceed 50% of my income?

This is common in high-cost cities and for individuals with significant medical expenses or student loan payments. Rather than abandoning the rule entirely, adjust your percentages to match your reality. A common adaptation is 60/20/20 or even 70/15/15. The goal is progress toward financial balance, not rigid adherence to percentages.

Should I include my employer’s 401(k) match in my savings calculation?

Yes, your employer match counts toward your 20% savings allocation. If you contribute 5% of your salary and your employer matches 4%, that’s 9% toward savings. However, be aware that your budget should be based on what comes from your paycheck—the match is “free money” that accelerates your savings rate.

How do I handle one-time or annual expenses with this budget?

Annual and one-time expenses should be budgeted monthly by dividing the total annual cost by 12. For example, if you pay $600 annually for car insurance, set aside $50 per month in a sinking fund. This prevents these expenses from derailing your monthly budget when they come due.

Can the 50/30/20 rule work for someone on a very low income?

The rule can work at any income level, though percentages may need adjustment. If your needs exceed 50% due to low income or high essential costs, focus on the core principle: spend less than you earn and consistently save something. Even 10% savings is valuable. As income increases, gradually shift toward the recommended percentages.

Should I include my spouse’s income separately or combined?

The 50/30/20 rule works best when applied to combined household income. This allows families to optimize their resources together rather than tracking individual spending separately. Discuss your combined goals and allocate dollars toward shared priorities.

Conclusion

The 50/30/20 budget rule offers a framework that adapts to nearly any financial situation. The examples in this article demonstrate how the rule scales across different incomes, family structures, and geographic locations—from the entry-level professional in Ohio to the high-earning software engineer in San Francisco.

The key to success isn’t perfection—it’s consistency and honest categorization. Start by understanding your true after-tax income, categorize your expenses accurately, and make incremental adjustments toward your target percentages. If your needs category runs slightly over 50% due to your specific circumstances, that’s okay. What matters is that you’re deliberately directing money toward both present enjoyment and future security.

Your next step: pull out your last three months of bank statements, calculate your actual after-tax income, and categorize your spending. You’ll quickly see where you stand relative to the 50/30/20 targets and what adjustments will make the biggest difference in your financial wellbeing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment